For Canadian business owners, saving isn’t just about setting money aside—it’s about doing it in a way that minimizes taxes, supports long-term growth, and aligns with your retirement and estate goals.

With multiple options available—from RRSPs and TFSAs to corporate structures and insurance strategies—choosing the right mix can significantly impact your financial future.

What are the best ways for business owners in Canada to save for retirement and reduce taxes?

The best savings strategies for Canadian business owners typically combine corporate savings, registered accounts (like RRSPs and TFSAs), and advanced planning tools such as holding companies, IPPs, and life insurance. The right mix depends on your income structure, long-term goals, and tax planning strategy.

If you’re unsure which savings strategies make the most sense for your situation, a structured review can help align your business income, tax planning, and long-term wealth goals.

Annuities

An annuity provides guaranteed income for life or a fixed period in exchange for a lump sum.

Pros:

- Guaranteed income regardless of market conditions

- No investment management required

Cons:

- Low flexibility—once purchased, funds are locked in

- No potential for capital appreciation

Estate and retirement considerations:

- Can be structured to provide income to a spouse after death

- Works well as a complement to other retirement savings

Best for: Business owners looking for guaranteed, passive retirement income

Canada Pension Plan (CPP)

CPP provides a stable, government-backed retirement income. As a business owner, you can choose to contribute or opt for dividends (which do not contribute to CPP).

Pros:

- Provides lifelong, indexed retirement income

- Disability and survivor benefits included

- Can be enhanced with additional contributions

Cons:

- Mandatory contributions reduce short-term cash flow

- Maximum pension benefits are limited

Estate and retirement considerations:

- Limited survivor benefits, meaning funds may not fully transfer to heirs

- Best for supplementing other retirement savings

Best for: Business owners wanting stable, indexed retirement income

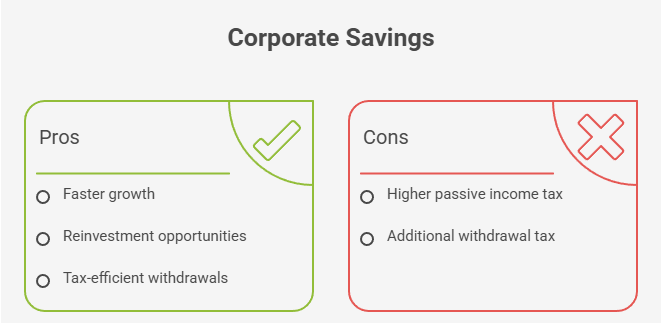

Corporate Savings

Many business owners leave excess profits in their corporation to take advantage of lower corporate tax rates.

Pros:

- Lower corporate tax rates allow savings to grow faster

- Retained earnings can be reinvested in the business or other assets

- Income can be withdrawn as dividends or salary based on tax planning

Cons:

- Passive income over $50,000 is taxed at a higher rate

- Personal withdrawals are subject to additional tax

Estate and retirement considerations:

- Corporate shares are subject to capital gains tax upon death unless structured properly

- Holding companies and estate freezes can reduce tax burdens

- Dividends provide flexible income in retirement but are taxed differently than capital gains

Best for: Business owners looking to defer personal taxes and reinvest profits

FHSA (First Home Savings Account)

The FHSA combines the tax benefits of an RRSP and TFSA to help first-time homebuyers.

Pros:

- Tax-deductible contributions

- Tax-free withdrawals for a home purchase

Cons:

- Must be used for a first home purchase

- Lifetime contribution limit of $40,000

Estate and retirement considerations:

- If unused, can be transferred to an RRSP without affecting contribution room

- Can help children or family members buy their first home

Best for: Business owners or their children saving for a first home

Holdco (Holding Company)

A holding company allows business owners to shelter investment income from personal taxes.

Pros:

- Lower corporate tax rate on investment income

- Can use accumulated funds to make investments, acquire assets, or fund future business ventures

- Helps with estate freezing and tax deferral

Cons:

- Complex structure with higher administration costs

- Taxes apply on dividends when distributed to personal accounts

Estate and retirement considerations:

- Transfer of assets to heirs may be more tax-efficient through Holdco

- Holdco can facilitate estate freezes to lock in the value of a business for tax purposes

Best for: Business owners looking to defer taxes and protect investments through a corporate structure

Individual Pension Plan (IPP)

An IPP is a defined benefit pension plan designed for incorporated business owners.

Pros:

- Higher contribution limits than RRSPs, especially for older individuals

- Contributions are tax-deductible to the corporation

- Creditor protection for pension assets

Cons:

- More complex and expensive to administer than an RRSP

- Locked-in funds with strict withdrawal rules

Estate and retirement considerations:

- IPP assets can be transferred to a spouse upon death

- Provides structured, predictable retirement income

- Avoids OAS clawback compared to RRSP withdrawals

Best for: Business owners over 40 who want structured retirement income

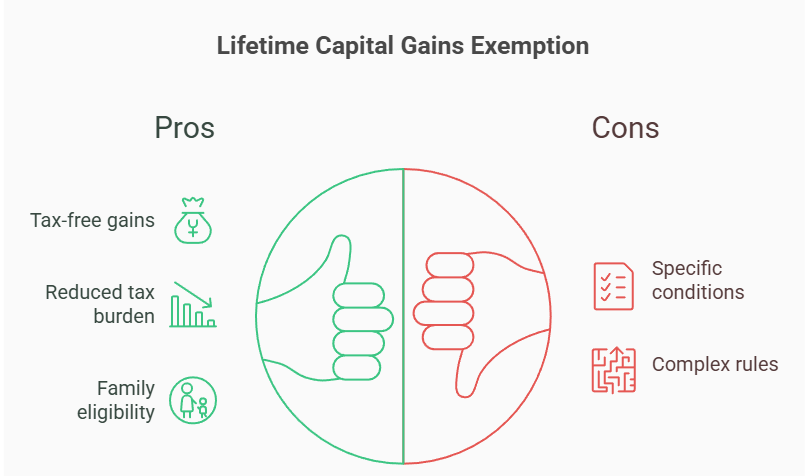

Lifetime Capital Gains Exemption

The Lifetime Capital Gains Exemption (LCGE) allows business owners to exclude up to $913,630 (2025 limit) of capital gains from taxation on the sale of qualifying small business shares, farm property, or fishing property.

Pros:

- Tax-free capital gains on qualifying shares

- Can significantly reduce tax burden upon selling a business or assets

- Available to both individuals and families

Cons:

- Must meet specific conditions to qualify (e.g., must have owned the shares for at least 24 months)

- Complex rules surrounding eligibility and claims

Estate and retirement considerations:

- Can be used to reduce taxes when transferring business ownership to heirs

- Planning ahead for the sale of a business is essential to maximize the LCGE

Best for: Business owners planning to sell or transfer their business and reduce capital gains tax

Personal Real Estate

Investing in real estate is a popular strategy for business owners looking to grow wealth outside of traditional investments.

Pros:

- Potential for long-term appreciation

- Rental income provides a steady cash flow

- Real estate can be used for personal or business purposes

Cons:

- Significant initial investment and ongoing maintenance costs

- Illiquid asset—difficult to access funds quickly

- Subject to capital gains tax upon sale (unless it’s the primary residence)

Estate and retirement considerations:

- Real estate can be a valuable estate planning tool for wealth transfer

- Transfer of real estate assets can be structured to minimize capital gains tax

- Can provide a source of income in retirement

Best for: Business owners seeking long-term growth and income diversification outside traditional savings options

Registered Education Savings Plan (RESP)

An RESP is a government-supported account for saving for a child’s education.

Pros:

- Government grants (20% on contributions, up to $7,200 per child)

- Tax-free investment growth until withdrawal

Cons:

- Withdrawals are taxable in the child’s hands

- Must be used for education, or taxes apply on unused funds

Estate and retirement considerations:

- Can be transferred to an RRSP if the child does not use it

- Helps reduce financial burden on future generations

Best for: Business owners saving for their children’s education

Registered Retirement Savings Plan (RRSP)

If you pay yourself a salary, RRSPs can be a great way to save for retirement while reducing your current tax bill.

Pros:

- Contributions reduce taxable income

- Investments grow tax-free until withdrawal

- Spousal RRSPs help with income splitting

Cons:

- Withdrawals are fully taxable

- Must convert to a RRIF by age 71 with required withdrawals

Estate and retirement considerations:

- Fully taxable upon death unless transferred to a spouse

- RRIF withdrawals impact government benefits like OAS

- Ideal for structured income in retirement

Best for: Business owners paying themselves a salary who expect lower taxes in retirement

Retirement Compensation Arrangement (RCA)

An RCA helps defer taxes on large payouts, such as bonuses or retirement packages.

Pros:

- Defers taxes on lump-sum payments

- Useful for high-income earners wanting to spread tax liability

Cons:

- 50% of contributions go into a refundable tax account with the CRA

- High administrative costs

Estate and retirement considerations:

- Tax-efficient estate planning strategy for business owners

- Helps avoid large tax hits on retirement payouts

Best for: Business owners expecting a large payout or needing tax deferral

Tax-Free Savings Account (TFSA)

Unlike RRSPs, TFSAs don’t offer a tax deduction, but all growth and withdrawals are tax-free.

Pros:

- Tax-free investment growth and withdrawals

- No mandatory withdrawals

- No impact on government benefits

Cons:

- Lower contribution limits than RRSPs

- No immediate tax deduction

Estate and retirement considerations:

- TFSAs pass tax-free to a spouse but not to other beneficiaries

- Ideal for emergency funds and flexible retirement income

Best for: Flexible, tax-free savings for retirement or unexpected expenses

Whole Life Insurance

Corporate-owned whole life insurance is a powerful tool for tax-free wealth transfer and estate planning.

Pros:

- Tax-sheltered investment growth

- Tax-free payout upon death

- Capital Dividend Account (CDA) allows tax-free distribution of insurance proceeds

Cons:

- Higher fees than traditional investments

- Less liquidity than other options

Best for: Tax-efficient estate planning and long-term asset protection

Summary

| Savings Option | Pros | Cons | Best For |

| Annuities | Guaranteed income, no market risk | Low flexibility, no capital appreciation | Guaranteed passive retirement income |

| Canada Pension Plan (CPP) | Lifelong income, disability benefits | Mandatory contributions, limited pension benefits | Stable, indexed retirement income |

| Corporate Savings | Tax deferral, reinvestment opportunities | Higher tax on passive income, personal withdrawal tax | Deferring personal taxes and reinvesting profits |

| FHSA (First Home Savings Account) | Tax-deductible, tax-free withdrawals for home purchase | Must be for first-time home, contribution limit of $40,000 | Saving for first-time home purchase |

| Holdco (Holding Company) | Tax deferral, investment income shelter, estate freeze | Higher admin costs, taxes on dividends | Protecting investments and structuring tax deferral |

| Individual Pension Plan (IPP) | Higher contribution limits, creditor protection | Expensive to administer, locked-in funds | Structured retirement income, especially for older business owners |

| Lifetime Capital Gains Exemption | Tax-free capital gains on qualifying shares | Must meet specific eligibility requirements | Business owners planning to sell or transfer their business |

| Registered Education Savings Plan (RESP) | Government grants, tax-free growth | Withdrawals taxable, must be used for education | Saving for children’s education |

| Registered Retirement Savings Plan (RRSP) | Tax deduction, tax-free growth | Fully taxable upon withdrawal, mandatory RRIF conversion | Saving for retirement while reducing current taxes |

| Retirement Compensation Arrangement (RCA) | Tax deferral, spreads tax liability | High administrative costs, refundable tax account with CRA | Business owners expecting large payouts |

| Tax-Free Savings Account (TFSA) | Tax-free growth, flexible withdrawals | Lower contribution limits, no tax deduction | Tax-free savings for retirement or unexpected expenses |

| Whole Life Insurance | Tax-sheltered growth, tax-free death benefit | High fees, less liquidity | Estate planning and wealth transfer |

Conclusion

Choosing where and how to save as a business owner isn’t just about returns—it’s about building a strategy that minimizes taxes, supports your retirement, and protects your wealth over time. A well-balanced approach that combines corporate and personal strategies can help you stay flexible while optimizing long-term outcomes.

The right structure can significantly reduce taxes and improve long-term wealth outcomes. Book a consultation with Purpose CPA to build a tax-efficient savings and retirement strategy tailored to you.