For Canadian business owners, deciding how to pay yourself—salary or dividends—is more than just a tax decision. It directly impacts your retirement income, cash flow, and long-term financial flexibility.

One of the biggest factors in this decision is the Canada Pension Plan (CPP). While salary triggers CPP contributions and future pension benefits, dividends provide more immediate cash flow and investment flexibility. Understanding the trade-offs is essential for building a strategy that aligns with your goals.

Should business owners take salary or dividends for CPP in Canada?

It depends on your goals. Salary provides access to CPP benefits, creating stable, inflation-adjusted retirement income. Dividends avoid CPP contributions, allowing more capital to be invested—but require discipline and carry investment risk. The best approach often involves balancing both strategies.

CPP Contribution Rates for 2026

The Canada Pension Plan (CPP) has two levels of contributions:

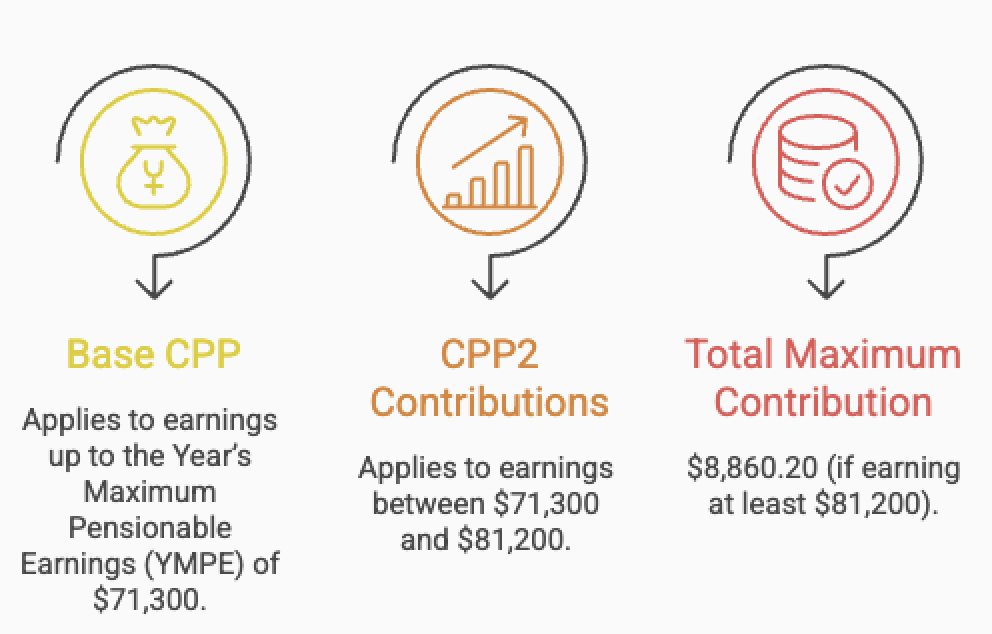

- Base CPP: Applies to earnings up to the Year’s Maximum Pensionable Earnings (YMPE) of $74,600.

- Contribution Rate (Employee & Employer each): 5.95%

- Total Contribution (Employee + Employer): $8,460.90

- CPP2 Contributions: Applies to earnings between $74,600 and $85,000.

- Contribution Rate (Employee & Employer each): 4.00%

- Total Contribution (Employee + Employer): $832.00

- Total Maximum Contribution (2026): $8,860.20 (if earning at least $9,292.90).

Paying yourself a salary also affects payroll obligations and compliance requirements.

Is CPP Sustainable Long-Term?

The CPP is currently considered well-funded, with the Canada Pension Plan Investment Board (CPPIB) managing a large portfolio of assets. The CPPIB aims for an annual return of around 4% above inflation to ensure sustainability. As of recent reports, the fund is projected to be sustainable for at least 75 years under current contribution and payout assumptions. However, future changes in demographics and economic conditions could impact its long-term viability.

If you’re unsure whether salary or dividends make more sense for your situation, a structured review can help you balance tax efficiency, retirement planning, and cash flow.

Salary vs Dividends: Key Trade-Offs

Taking a Salary & Paying into CPP

| Pros | Cons |

| Builds CPP retirement benefits (guaranteed, inflation-adjusted income) | Higher payroll taxes (11.9% total CPP for self-employed) |

| Creates RRSP contribution room | Lower flexibility (must wait until age 60+ for CPP benefits) |

| Helps qualify for mortgages | CPP returns may be lower than private investments |

| Provides creditor protection for CPP pension | Potential for OAS clawbacks due to higher taxable income |

| Estate planning advantages (CPP survivor benefits) |

Taking Dividends & Investing the CPP Savings

| Pros | Cons |

| No CPP deductions (keep the extra 11.9% and invest it yourself) | No CPP pension—retirement depends on personal savings |

| More control over investments (higher potential returns than CPP) | Higher investment risk—markets fluctuate, while CPP is stable |

| Dividends are taxed at a lower rate than salary | Requires financial discipline to invest the savings |

| Reduces taxable income (potentially avoiding OAS clawbacks) | No CPP survivor benefits for estate planning |

If reinvesting the savings in a corporation can generate an annual return of 4-8%, the long-term benefits may exceed those of CPP, assuming disciplined investment and risk management. Dividends are often used as part of a broader tax planning strategy for business owners.

Reinvesting CPP Savings for a 4-8% Return

Business owners who choose dividends over salary avoid CPP contributions, freeing up additional cash flow. If this savings is reinvested effectively, it could potentially generate better retirement income than CPP.

How Reinvesting Works

- The 11.9% of earnings that would have gone to CPP can instead be invested in stocks, bonds, private equity, or corporate assets.

- A well-balanced portfolio with a target return of 4-8% annually could yield significantly higher retirement savings than CPP payouts.

- Business owners can leverage tax-efficient investment strategies, such as corporate investment accounts or tax-exempt insurance policies, to optimize growth.

Potential Growth Comparison

| Investment Return Rate | Value After 40 Years (Starting with $8,860/year) |

| 4% | ~$1.1 million |

| 6% | ~$1.9 million |

| 8% | ~$3.3 million |

By contrast, the total estimated lifetime CPP payout (assuming living to age 85) would be around $550,000–$650,000. This means that disciplined reinvestment could provide significantly greater financial security if managed properly.

Risks to Consider

- Market fluctuations may impact investment returns.

- Lack of CPP contributions means no guaranteed pension or survivor benefits.

- Requires financial discipline to reinvest rather than spend the savings.

- Higher portfolio returns may be subject to capital gains tax.

Understanding your financial performance is key to evaluating whether investment returns outperform CPP.

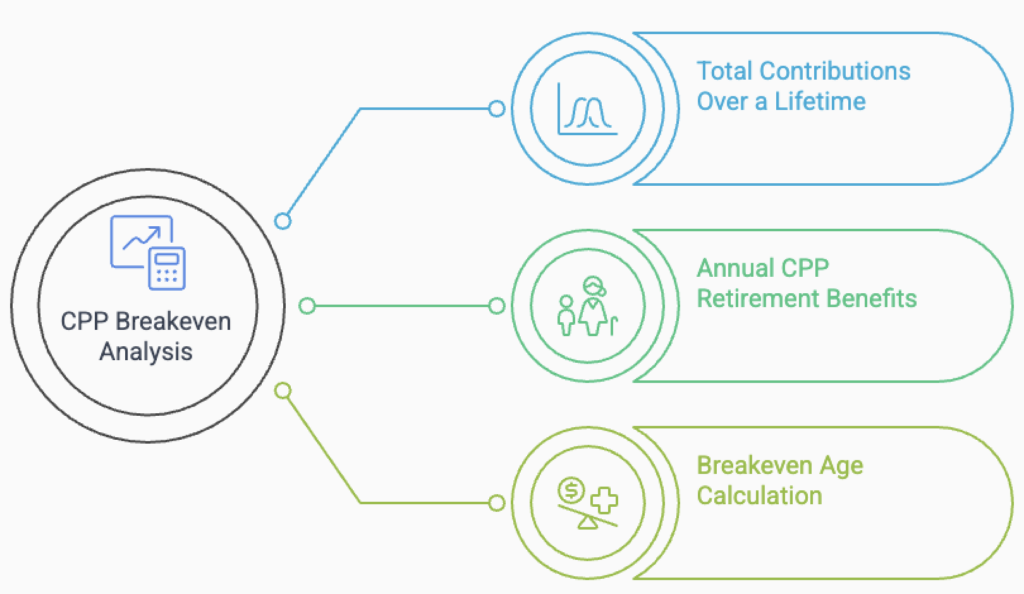

CPP Breakeven Analysis: When Do You Get Your Money Back?

The breakeven point is the age at which total CPP benefits received equal total contributions made (employee + employer + CPP2).

Total Contributions Over a Lifetime

Assuming 40 years of maximum CPP contributions (ages 25-65):

- Annual Contribution (2026 rates): $9,292.90

- Total Lifetime Contributions: $371,716

Annual CPP Retirement Benefits

- CPP at 65 (2026 max): ~$1,440/month (~$17,300/year)

- Adjusted for CPP2: ~$19,000/year

Breakeven Age Calculation

- $371,716 ÷ $19,000/year ≈ 19.6 years

- Breakeven Age = 65 + 19.6 ≈ 85 years old

If living past 85, CPP contributions provide more in benefits than was paid in. Those who do not reach this age may not fully recover their contributions. Long-term planning decisions like this should align with your overall wealth and retirement strategy.

Conclusion

There is no one-size-fits-all answer when it comes to salary vs dividends. The right approach depends on your risk tolerance, retirement goals, and financial discipline. CPP provides stability and guaranteed income, while dividends offer flexibility and potential for higher returns. A well-planned strategy often combines both to optimize long-term outcomes.

The right strategy can significantly impact your taxes, retirement income, and financial flexibility. Book a consultation with us to build a personalized compensation and retirement strategy.