Employment Insurance (EI) can provide valuable financial support—but for business owners in Canada, the rules are not always straightforward. Whether you’re self-employed or incorporated, your obligation to pay EI (and whether it’s worth it) depends on how your business is structured and how you pay yourself.

Understanding when EI is required, when you’re exempt, and whether opting in makes financial sense can help you avoid unnecessary costs and make more informed planning decisions.

Do Business Owners Need to Pay EI in Canada?

It depends on your business structure. Sole proprietors and partners are not required to pay EI but can opt into special benefits. Incorporated business owners who own more than 40% of their company are exempt, while those owning 40% or less must pay EI and are eligible for regular benefits.

Whether you must pay EI depends on your business structure and ownership percentage.

Self-Employed Individuals (Sole Proprietors & Partnerships)

- EI is not required because self-employed individuals are not considered employees.

- However, they can voluntarily opt into EI Special Benefits to access maternity, parental, sickness, and caregiving benefits.

Incorporated Business Owners (Shareholder-Employees)

- If you own more than 40% of the voting shares in your corporation, you are exempt from EI.

- If you own 40% or less, you are treated as a regular employee and must pay EI premiums on your salary.

How you structure ownership and compensation can significantly impact not only EI, but your overall tax strategy.

Employer Contributions

- If you are required to pay EI as an employee, your corporation must also pay the employer portion (1.4 times the employee rate).

- If you are exempt, your corporation does not pay EI premiums either.

If you’re unsure whether you should be paying EI—or whether opting in makes sense—a professional review can help you evaluate your structure, reduce unnecessary costs, and align your strategy with your long-term goals.

Can Incorporated Business Owners Enroll in EI Special Benefits?

Who Can Enroll?

- Only self-employed individuals (sole proprietors, partners, and incorporated individuals who do not pay themselves a salary) can opt into the EI Special Benefits program.

- If you are an incorporated business owner who pays yourself a salary, you cannot enroll in EI Special Benefits. Instead, you are subject to regular EI rules (mandatory if you own 40% or less, exempt if you own more than 40%).

Do Owners Need to Pay the Employer Portion?

- No, self-employed individuals who enroll in the EI Special Benefits program only pay the employee portion of EI (1.66% in 2025).

- Since they do not have an employer, they do not need to pay the employer portion (2.32%).

- However, once enrolled, they must continue paying EI premiums for as long as they are self-employed.

Payroll obligations like EI, CPP, and remittances must be handled accurately to avoid penalties.

EI Special Benefits for Self-Employed Business Owners

For self-employed professionals or exempt shareholder-owners, the government offers an opt-in program for EI Special Benefits.

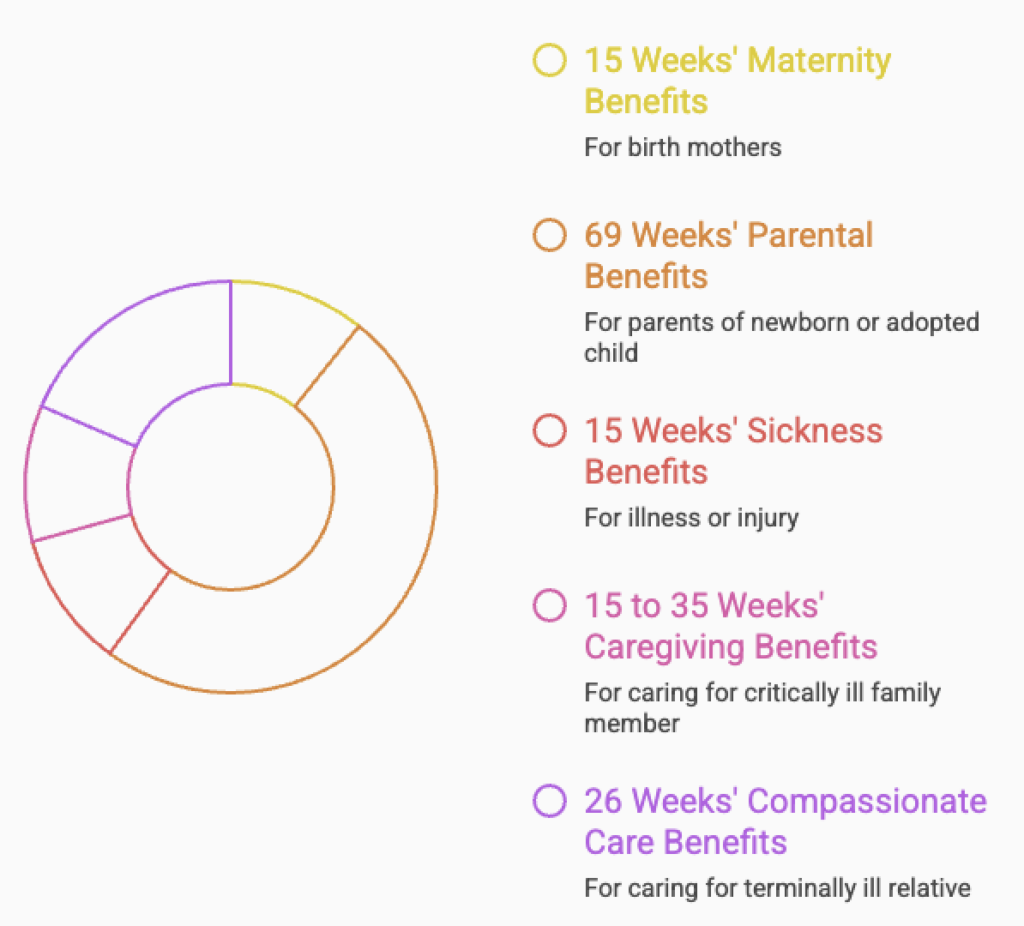

What Benefits Can You Get?

By enrolling, you gain access to:

- Maternity Benefits – 15 weeks (for birth mothers)

- Parental Benefits – Up to 69 weeks (for parents of a newborn or adopted child)

- Sickness Benefits – 15 weeks (if unable to work due to illness or injury)

- Caregiving Benefits – 15 to 35 weeks (for caring for a critically ill family member)

- Compassionate Care Benefits – 26 weeks (for caring for a terminally ill relative)

How Much Does It Cost?

- You pay 1.66% of your net self-employment income, up to a maximum of $1,049.12 per year (2025).

- Benefits are paid at 55% of your average weekly earnings, up to $668 per week.

Is Paying EI Worth It for Business Owners?

Since EI is mandatory for some business owners but optional for others, let’s look at whether it makes financial sense to pay in.

If You Are Required to Pay EI (40% Ownership or Less)

- You must pay 1.66% of your salary into EI, and your corporation must match with 2.32%.

- This provides access to EI regular benefits (if you lose your job) and EI special benefits (maternity, sickness, etc.).

- If you never need EI, your contributions are a sunk cost.

If You Are Exempt from EI (More than 40% Ownership)

- You can opt in voluntarily to EI Special Benefits but not to regular EI.

- The breakeven depends on whether you expect to take time off for parental leave, sickness, or caregiving.

Breakeven Calculation

Assuming an owner enrolls in EI at age 30 and retires at 60, contributing only the employee portion, they would pay $31,473.60 over 30 years. If they take one sickness leave (15 weeks), one parental leave (40 weeks), and one caregiving leave (26 weeks), they would receive $54,108 in benefits, resulting in a net gain of $22,634.40. This suggests that enrolling in EI could be financially beneficial if only the employee portion is considered. However, if the employer portion is included, total contributions rise to $75,502.20, leading to a net loss of $21,394.20, making enrollment less worthwhile.

What If You Accidentally Paid EI as an Exempt Business Owner?

If you own more than 40% of the company but still paid EI premiums over the years, you may be eligible for a refund from the CRA.

Steps to Get a Refund

- Apply for a Refund (Up to 3 Years Back)

- Submit Form PD24 – EI Premium Refund Application (Download Here).

- Provide proof of your shareholder status and past T4 slips.

- Employer Portion Refund

- Your corporation may also apply for a refund of the employer-paid EI premiums.

Refunds are only available for the last three years, so it’s best to apply as soon as possible. If you have claimed EI benefits during this period, you may not be eligible for a refund.

Conclusion

EI rules for business owners are nuanced and depend heavily on ownership structure, compensation, and long-term planning goals. While some are required to contribute, others have the flexibility to opt in—or avoid EI altogether. Understanding these rules can help you make better decisions about cash flow, risk protection, and overall financial strategy.

A small adjustment in how you structure your compensation could lead to meaningful savings. Book a consultation with us to review your payroll setup and optimize your tax strategy.