")

Tax planning is one of the most effective ways for Canadian small business owners to keep more of what they earn while staying compliant with CRA requirements. But beyond simply filing taxes, strategic planning involves structuring income, maximizing deductions, and making informed financial decisions throughout the year.

Whether you operate as a sole proprietor or through a corporation, the right tax strategy can improve cash flow, reduce risk, and support long-term financial growth.

How can Small Business Owners Reduce Taxes in Canada?

Small business owners in Canada can reduce taxes by claiming eligible expenses, optimizing salary vs. dividend compensation, using tax-efficient accounts, and structuring their business properly. Effective tax planning also includes managing GST/HST, tracking expenses accurately, and planning ahead for income and investments.

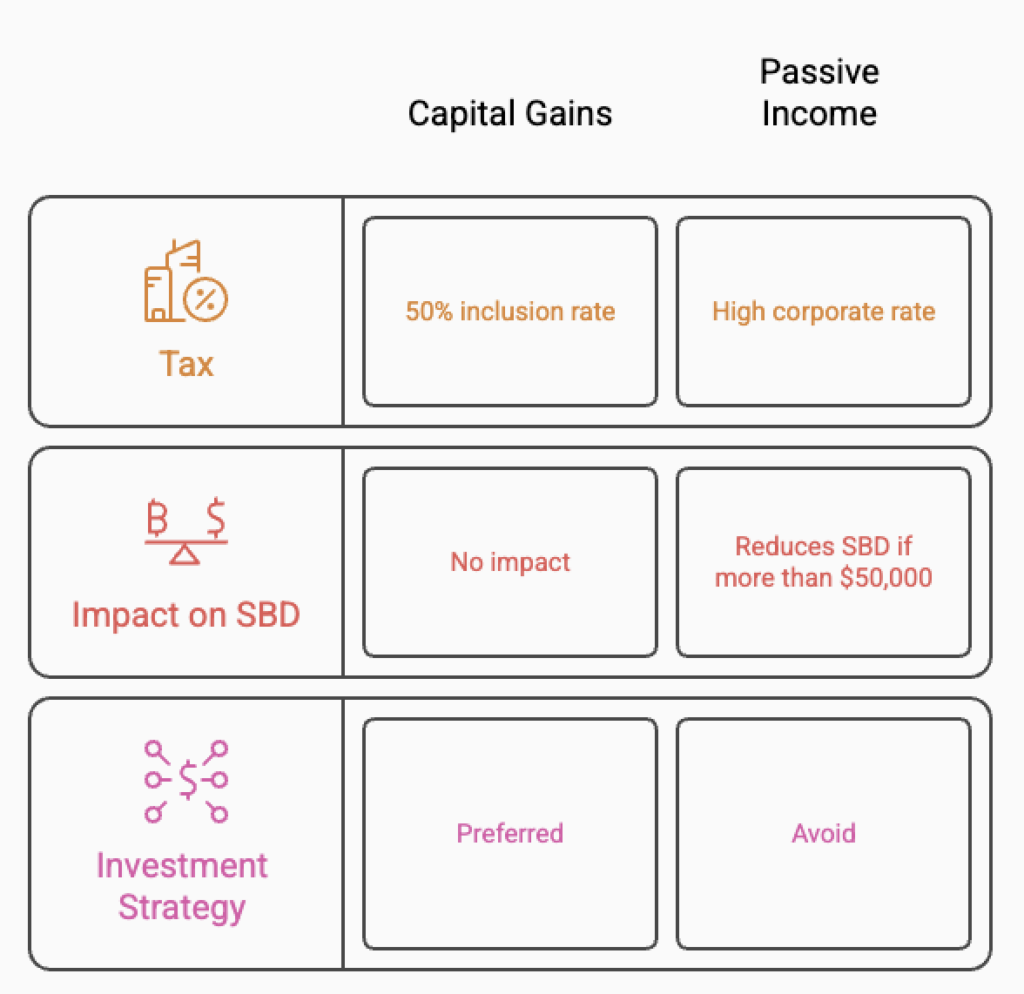

Capital Gains vs. Passive Income

Understanding the tax treatment of capital gains versus passive income is crucial for incorporated business owners.

Key Considerations:

- Capital gains benefit from a 50% inclusion rate, meaning only half of the gain is taxable.

- Passive income (e.g., rental income, investment income) is taxed at a high corporate tax rate, reducing the Small Business Deduction (SBD) if passive income exceeds $50,000.

- Investing excess business profits in assets that generate capital gains rather than passive income can reduce overall corporate tax liability.

Childcare Expenses

If you run a business and have children, you may be eligible to claim childcare expenses, reducing your taxable income. The CRA allows you to deduct expenses related to daycare, nannies, and babysitters, as long as the care is required for you (or your spouse) to earn business income.

Key Considerations:

- The lower-income spouse must typically claim the deduction.

- The maximum claimable amounts are:

- $8,000 per child under 7

- $5,000 per child aged 7 to 16

- $11,000 per child with a disability

- Expenses must be supported by receipts with the caregiver’s name, address, and SIN (if applicable).

Proper documentation is essential to ensure these claims are accepted in case of an audit.

Company-Owned Vehicle & Standby Charge

If your corporation owns a vehicle that you use personally, a standby charge may apply, increasing your taxable income.

Key Considerations:

- 2 percent of the vehicle’s cost per month if purchased

- Two-thirds of the lease cost per month if leased

- Reducing personal use and tracking mileage can help minimize this taxable benefit.

Using business assets for personal purposes can create additional taxable benefits if not tracked properly.

Corporate-Owned Life Insurance

A corporation can own a life insurance policy, providing tax advantages for both the business and shareholders.

Benefits:

- Premiums are not deductible, but the death benefit is paid out tax-free.

- The capital dividend account (CDA) allows for tax-free withdrawals of the insurance proceeds.

- It can be used as collateral for financing, improving cash flow.

If you’re unsure whether you’re taking full advantage of available tax strategies, a professional review can help identify missed opportunities and ensure your approach is aligned with your business goals.

Employee-Paid Insurance Premiums (LTD, CI, AD&D)

The tax treatment of insurance benefits depends on who pays the premiums.

Key Considerations:

- Employee-paid LTD ensures disability benefits are tax-free.

- Employer-paid LTD makes benefits taxable.

- Employee-paid CI and AD&D benefits are tax-free.

Having employees pay their own LTD premiums is generally the most tax-efficient option.

GST Input Tax Credits (ITCs)

If your business is GST/HST registered, you can claim back the GST you paid on eligible expenses through ITCs.

Eligible Expenses:

- Office rent and utilities

- Professional services (legal, accounting)

- Business-related travel expenses

- Equipment and supplies

Keeping organized receipts and proper records ensures you can fully benefit from ITCs. Understanding when GST/HST applies—and when it doesn’t—is key to avoiding reporting errors.

Health Spending Allowance (HSA)

An HSA allows incorporated business owners to cover personal medical expenses tax-free.

Benefits:

- 100 percent tax-deductible for the business

- No personal taxable benefit if structured correctly

- Covers a wide range of medical, dental, and vision expenses

An HSA is particularly valuable for business owners who do not have traditional health benefits.

Home Office Expenses

If you operate your business from home, you may be able to deduct a portion of your home expenses.

Eligible Expenses:

- Rent or mortgage interest

- Utilities (electricity, heat, water, internet)

- Property taxes and home insurance

- Repairs and maintenance related to the office space

Your deduction is based on the percentage of your home used for business.

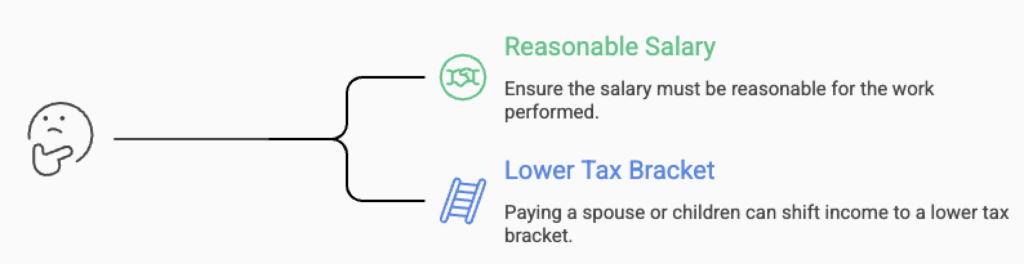

Income Splitting

Income splitting involves paying a reasonable salary to family members who work in your business, reducing the overall tax burden.

Key Considerations:

- The salary must be reasonable for the work performed.

- Paying a spouse or children can shift income to a lower tax bracket.

Maximizing Business Expenses Paid Personally

Many business owners pay expenses personally without realizing they could be reimbursed by the business, reducing taxable income.

Best Practices:

- Use a business credit card to track expenses.

- Submit monthly expense reports to reimburse yourself from the company.

Mileage Allowance

If you use your personal vehicle for business purposes, you can claim mileage as a tax deduction.

Key Considerations:

- The CRA’s 2025 mileage rates:

- 72 cents per kilometer for the first 5,000 kilometers

- 66 cents per kilometer after that

- Keeping a detailed mileage log is essential.

Choosing between a company-owned vehicle and personal reimbursement can significantly impact your tax outcome.

Conclusion

Effective tax planning goes beyond filing—it’s about making proactive decisions that reduce your tax burden while supporting long-term growth. By understanding available deductions, structuring income properly, and maintaining accurate records, you can significantly improve your financial position.

Even small adjustments can lead to meaningful tax savings over time. Book a consultation with Purpose CPA to review your tax strategy and identify opportunities to reduce taxes and improve cash flow.