Whether you operate as an incorporated business owner or a sole proprietor, personal tax planning is where we most often see money left on the table. Many business owners focus heavily on business expenses and year-end taxes, assuming their personal return will “sort itself out.” In reality, personal deductions, credits, and planning decisions often determine whether tax season ends with a refund — or a surprise balance owing.

Below are the most common personal tax deductions business owners miss, how they apply to both incorporated owners and sole proprietors, and why they matter.

Childcare Expenses

Childcare expenses are one of the most valuable personal tax deductions available to business owners — regardless of structure.

Eligible costs may include:

- Daycare and preschool

- Before-and-after school care

- Day camps

Key considerations:

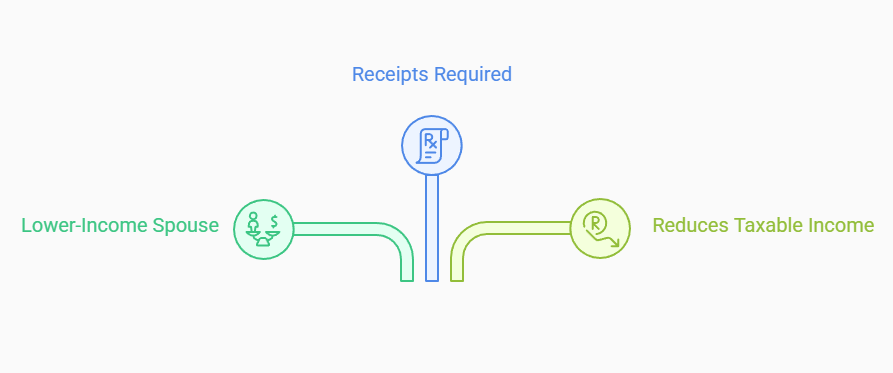

- Typically claimed by the lower-income spouse

- Requires receipts with the provider’s SIN or business number

- Reduces taxable income directly

For sole proprietors, childcare is often overlooked because business and personal expenses feel blended. For incorporated owners, it’s frequently missed because focus stays on corporate deductions only.

Charitable Donations Over $200

Many business owners donate personally or through their corporation, but fail to coordinate the tax impact.

What to consider:

- Donation credits increase once annual donations exceed $200

- Donations can be carried forward for up to five years

- Personal versus corporate donations should be planned intentionally

Claiming donations personally is often more effective when personal income is higher, while corporate donations may make sense when funds are retained in the company.

Home Office Expenses

Home office expenses apply differently depending on structure, but remain relevant for both incorporated owners and sole proprietors.

- Sole proprietors may deduct home office expenses directly against business income

- Incorporated owners may deduct via reasonable expense allocations or reimbursements

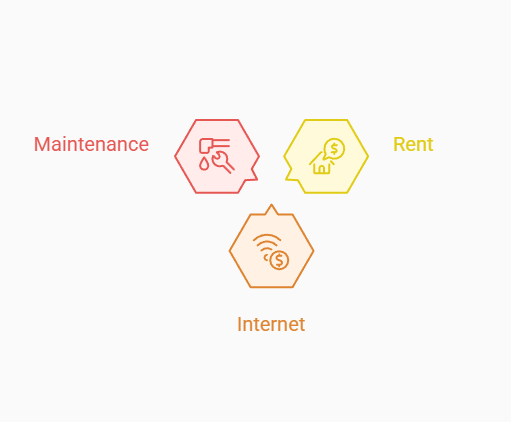

Eligible costs may include:

- A portion of rent, utilities, or mortgage interest

- Internet costs

- Workspace-related maintenance

Improper allocation or missing documentation is one of the most common issues we see during CRA reviews. At this point, many business owners start to realize the issue isn’t whether deductions exist — it’s whether anyone is looking at personal and business taxes together, instead of in isolation.

Medical Expenses

Medical expenses are often overlooked because they’re paid sporadically and not tracked intentionally.

Eligible expenses may include:

- Dental and orthodontic work

- Prescription glasses and contact lenses

- Therapy and psychological services

- Private health insurance premiums

Medical expenses are most effective when grouped into a strategic 12-month period, particularly in higher-income years.

Dependent Medical Expenses

In addition to your own medical costs, business owners may also claim medical expenses paid for dependents.

This can include:

- Children

- Aging parents or grandparents

- Financially dependent relatives

These expenses are often paid informally and spread across family members, making them easy to miss — despite being fully eligible when documented properly.

Union and Professional Dues

Certain professional and regulatory dues remain personally deductible for both incorporated owners and sole proprietors.

Examples include:

- Regulatory body dues

- Mandatory professional associations

- Licensing or trade organizations

Optional networking groups or social memberships generally do not qualify.

Example: How Much Tax Savings Is Left on the Table?

Profile

- Incorporated owner or sole proprietor

- British Columbia resident

- Total personal income: $100,000

- Approximate marginal tax rate: 38%

Expenses Paid During the Year

| Expense | Amount |

| Childcare | $9,500 |

| Charitable donations | $1,500 |

| Home office & allocable costs | $3,000 |

| Professional dues | $1,200 |

| Medical & dependent medical expenses | $2,500 |

Estimated Tax Impact

- Deductions (childcare, home office, dues):

$13,700 × 38% ≈ $5,200 in tax savings - Non-refundable credits (donations and medical):

≈ $700–$800 in tax savings

Total Estimated Personal Tax Savings Missed

Approximately $6,000 These are not aggressive strategies — they are legitimate expenses already paid, simply not planned intentionally.

Why Business Owners Miss These Deductions

We commonly see missed deductions because:

- Personal and business planning are treated separately

- Dividend or draw decisions aren’t coordinated with personal tax

- Expenses aren’t tracked consistently during the year

- Tax filing is treated as compliance rather than strategy

This applies just as much to sole proprietors as it does to incorporated owners.

Bonus Tip #1: Use a T1213 to Improve Cash Flow

While not a deduction, a T1213 Request to Reduce Tax Deductions at Source can materially improve cash flow.

If you regularly claim deductions or make RRSP contributions, CRA may approve reduced tax withholding on other personal income.

Why this matters:

- More cash flow throughout the year

- Less reliance on refunds

- Better alignment between tax paid and tax owed

Bonus Tip #2: Plan Deductions to Offset Dividend or Draw Tax at Filing Time

One of the most common surprises business owners face is unexpected personal tax owing.

- Incorporated owners often pay dividends without source deductions

- Sole proprietors often underestimate tax on draws

Without planning, this can result in a large balance owing at tax time. Strategically planning personal deductions — such as childcare, medical expenses, donations, and RRSP contributions — can help offset tax created by dividends or business income, smoothing cash flow and reducing year-end stress.

Bonus Tip #3: Use RRSP Contributions to Drop Into the Next Tax Bracket

Many business owners have RRSP contribution room but limited cash to fully maximize it. In these cases, the goal doesn’t need to be “max out the RRSP” — it can simply be dropping into the next marginal tax bracket.

Example at $100,000 of Income

- Personal income: $100,000

- Marginal tax rate on the top portion: ~38%

- Next marginal tax bracket: ~31%

By contributing just enough RRSP to reduce taxable income to the next bracket — for example, $5,000 — the tax impact can be meaningful:

- $5,000 × 38% ≈ $1,900 in immediate tax savings

This approach:

- Requires less cash than maxing out RRSPs

- Reduces tax owing at filing time

- Works especially well when dividends or business income create a surprise balance owing

For many business owners, this is a practical middle ground between “no RRSP” and “fully maximizing RRSPs.”

Conclusion

Whether you’re incorporated or operating as a sole proprietor, effective tax planning doesn’t stop at your business income. Personal deductions, income timing, and cash flow planning are just as important — and often where the easiest wins are found.

If this article raised questions about how your personal and business taxes fit together, that’s usually a sign something hasn’t been reviewed holistically. Contact us today to help connect the dots—so nothing legitimate gets missed.