")

As a growing Canadian business, securing bank financing can be a crucial step in achieving your goals. Whether you need capital for expansion, purchasing new equipment, or improving cash flow, preparing well can significantly improve your chances of securing a loan with favourable terms. Here’s a step-by-step guide to help you get ready to apply for a loan and successfully secure financing for your business.

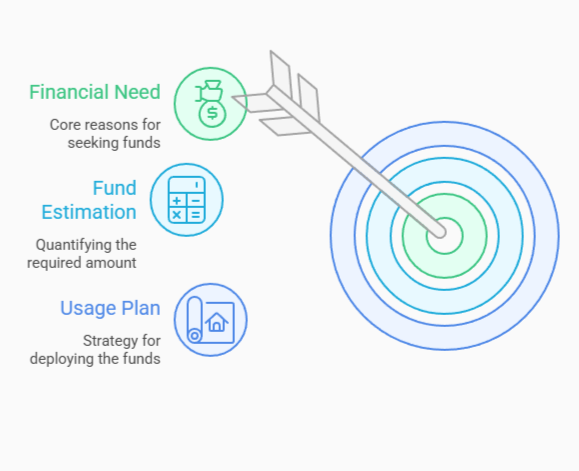

1. Assess Your Financial Needs and Objectives

Before you apply for a loan, it’s essential to have a clear understanding of the purpose of the financing. Do you need funds for expansion, buying equipment, or covering cash flow gaps? Estimate exactly how much you need and develop a plan for how you will use the money. This will help you select the right type of loan and show the bank that you have a structured plan.

2. Develop a Comprehensive Business Plan

A well-drafted business plan is essential when applying for a loan. Your business plan should include:

- Executive Summary: A brief overview of your business, its mission, and goals.

- Market Analysis: Understanding your market, competitors, and growth potential.

- Operational Plan: How your business operates on a day-to-day basis.

- Financial Projections: Projected income statements, balance sheets, and cash flow for the next 1-3 years.

- Use of Funds: A clear breakdown of how the loan will be used.

If you’re unsure about the details, a qualified accountant can be invaluable in helping you fine-tune your financial projections and ensuring your business plan is comprehensive and realistic.

3. Understand Your Creditworthiness

Canadian lenders will evaluate both your personal and business credit scores. Before applying for a loan, check both scores and make sure they are in good standing. If there are any issues, take steps to resolve them before applying. Keep in mind that banks may also require a personal guarantee, especially for smaller or newer businesses, so be transparent about your credit history.

4. Gather Financial Statements and Documents

Banks will require a number of documents to assess your financial health. Prepare the following:

- Balance Sheets: To show your business’s financial standing.

- Income Statements: To demonstrate your revenue, expenses, and profitability.

- Cash Flow Statements: To provide insight into your cash inflows and outflows.

- Tax Returns: Be prepared to provide your business’s tax returns for the last 2-3 years.

- Bank Statements: To show liquidity and financial activity.

An accountant can help ensure that these documents are accurate, up-to-date, and prepared in the format that banks prefer.

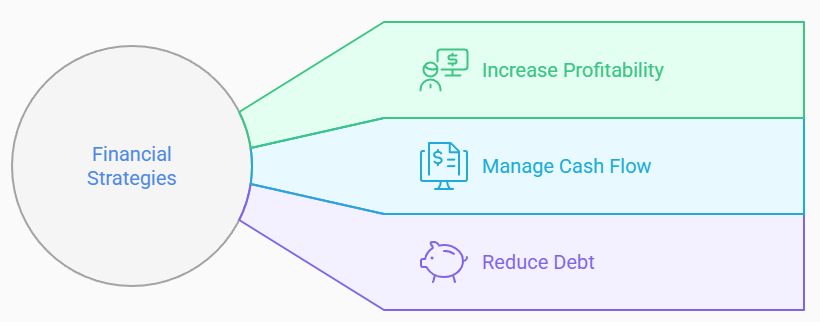

5. Ensure Strong Business Financials

Lenders want to see that your business is financially stable and able to repay the loan. To prepare:

- Increase Profitability: Work on improving your profits by cutting unnecessary costs and increasing revenue.

- Manage Cash Flow: Ensure you can generate enough cash to cover loan repayments. Demonstrating solid cash flow is key to securing financing.

- Reduce Debt: Banks may hesitate to lend if your business has too much debt. Reducing outstanding debt will improve your chances of approval.

A qualified accountant can help you optimize your business’s financials and provide advice on managing costs, improving profitability, and maximizing cash flow.

6. Prepare Collateral (if Required)

Some loans may require collateral, such as property, equipment, or inventory. Identify any assets you could pledge to secure the loan. Ensure that these assets are properly valued and documented. If you’re unsure about the value of your assets, an accountant can help assess them and provide accurate documentation.

7. Build Relationships with Your Bank

Start building a relationship with your bank before applying for financing. This can help create trust and make the loan application process smoother. Consider meeting with a business banker to discuss your goals and financing needs. It’s also beneficial to have a strong history with your bank, so consider maintaining accounts or services with them.

8. Prepare a Loan Repayment Plan

Banks want to see that you have a plan for repaying the loan. Create a repayment schedule that shows how your business will manage loan payments without negatively affecting day-to-day operations. Include this in your business plan and financial projections.

9. Evaluate Financing Options

Research the different types of loans available for Canadian businesses. Some common options include:

- Term Loans: Best for large, one-time expenses like purchasing equipment or expanding your business.

- Lines of Credit: Ideal for managing cash flow on a regular basis or covering unexpected expenses.

- SBA Loans: The Canadian version, such as the Canada Small Business Financing Program (CSBFP), provides favourable loan terms for businesses that meet certain criteria.

- Equipment Financing: For businesses that need to purchase new equipment, this option allows you to borrow specifically for that purpose.

Compare interest rates, repayment terms, and fees associated with each type of financing to ensure you select the best option for your needs.

10. Prepare for Questions

Your bank will likely ask detailed questions about your business. Be prepared to answer questions about your company’s risks, opportunities, and how the loan fits into your overall business strategy. Transparency is key—if your business faces challenges, explain how you plan to address them.

11. Consider a Co-Signer or Partner

If your credit history is less-than-ideal, consider having a co-signer or business partner with stronger financials. This can improve your chances of securing a loan, especially for small businesses or startups.

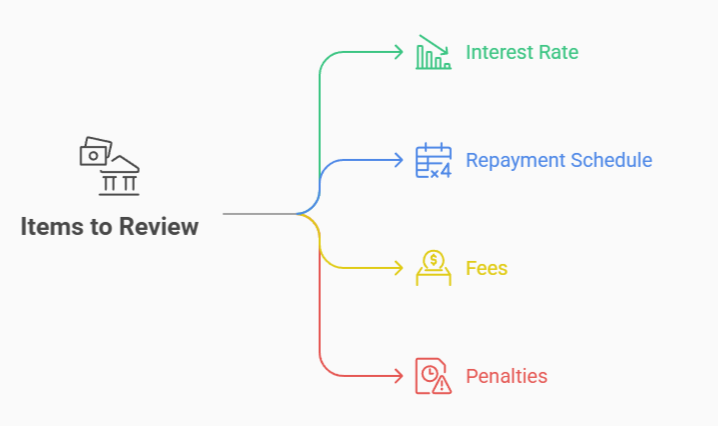

12. Review Loan Terms Carefully

Once you receive an offer, make sure to review all terms carefully. Look at the interest rate, repayment schedule, fees, and any penalties for late payments or early repayment. If necessary, negotiate the terms to ensure the loan is manageable and suits your business needs.

Conclusion

Navigating the loan application process can be complex, but you don’t have to do it alone. An experienced accountant can help ensure that your financials are in order, refine your projections, and offer guidance on loan options. Ready to take the next step in growing your business? Contact us today for expert advice and assistance in securing financing for your business.