")

Do you know there is a tool that can help self-employed business owners transfer business assets to a corporation in exchange for shares, deferring taxes on capital gains? The Section 85 rollover in Canada enables incorporation, protects personal assets, and supports future tax planning. Filing the T2057 form with the CRA is required, and professional advice ensures compliance and maximizes benefits.

What is a Section 85 Rollover?

A Section 85 rollover is a tax-deferred transfer mechanism under the Income Tax Act (Canada).

It allows self-employed business owners or individuals to transfer certain assets, such as those in a sole proprietorship or partnership, to a corporation in exchange for shares of the corporation, without triggering immediate tax consequences on the asset’s accrued gains.

Transferring assets into a corporation isn’t just a formality—without proper planning, it can trigger immediate tax consequences. Section 85 can defer those taxes, but only if it’s structured and filed correctly. A quick review can help you determine whether a rollover is appropriate and ensure it’s implemented properly from the start.

Purpose

- To incorporate a business while deferring taxes on gains associated with the transferred assets.

- Ensures continuity of ownership while transitioning from an unincorporated to an incorporated structure.

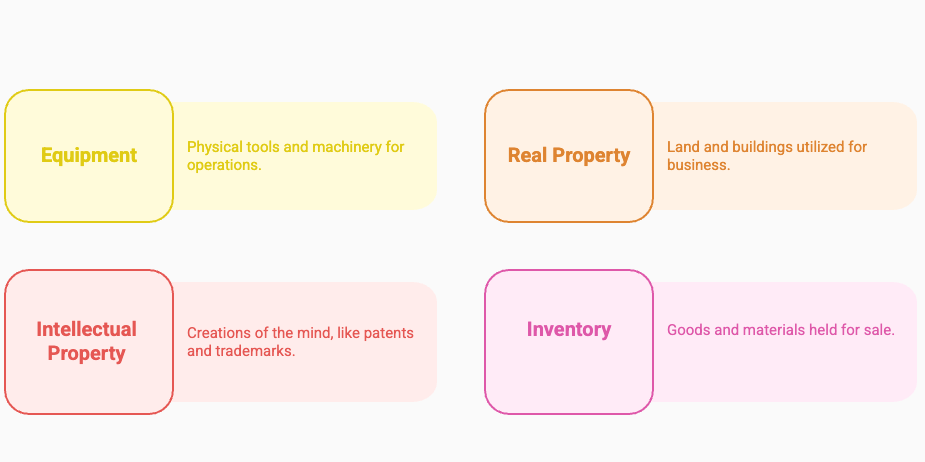

Eligible Assets

Common eligible assets include:

- Equipment

- Real property (used in the business)

- Intellectual property

- Inventory

Note: Accounts receivable and certain liabilities may also be transferred, but cash cannot be rolled over.

How Does the Rollover work?

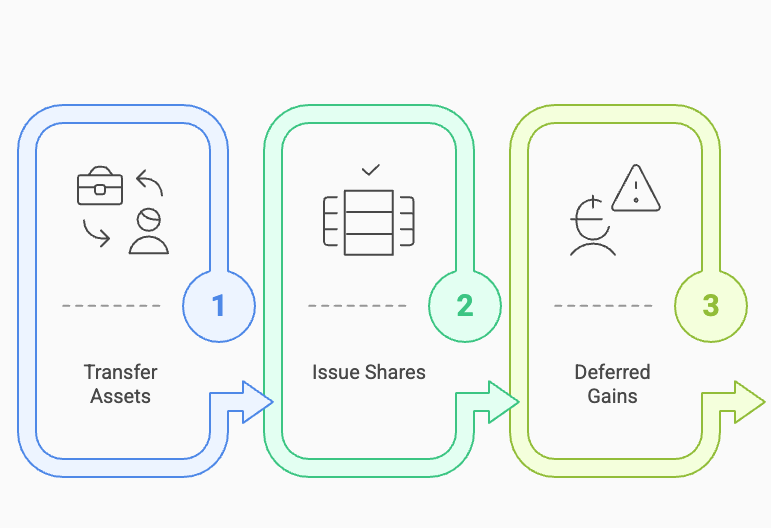

- You transfer the assets to the corporation at an agreed-upon value (usually the tax cost or a negotiated value between tax cost and fair market value).

- The corporation issues shares to you (or a combination of shares and other consideration like promissory notes).

- Any taxable gains on the difference between the adjusted cost base (ACB) of the asset and its fair market value (FMV) can be deferred.

Tax Deferral

- The tax is not eliminated; it is deferred until a later event (e.g., sale of shares or the business).

- The “rollover amount” or “elected amount” determines how much gain, if any, is recognized at the time of transfer.

Legal Requirements

- A Section 85 election form (T2057) must be filed with the Canada Revenue Agency (CRA). This outlines the details of the transfer, the elected amount, and other specifics.

- Both the individual and the corporation must sign the form.

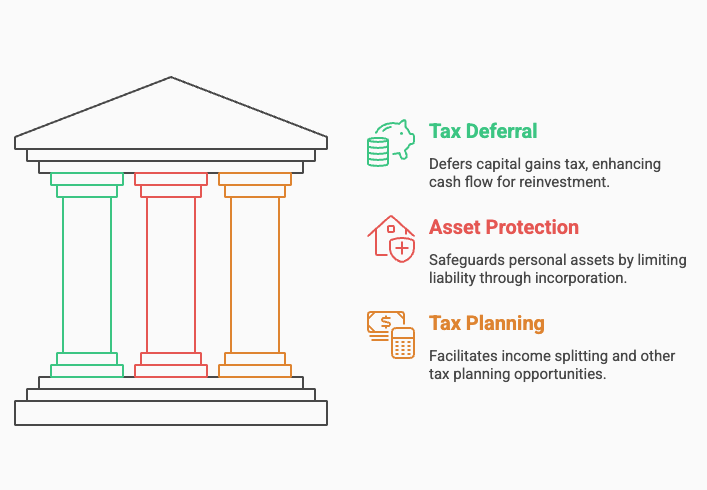

Why Carry Out a Section 85 Rollover?

- Defers capital gains tax, improving cash flow for reinvestment.

- Protects personal assets by limiting liability through incorporation.

- Allows for income splitting or other tax planning opportunities in a corporate structure.

What are the Tax Considerations?

- Proper valuation of assets is critical to avoid disputes with the CRA.

- Legal and accounting fees are typically incurred to ensure the transfer is compliant and tax-efficient.

- Future tax planning is required to optimize the eventual sale or disposition of shares.

Conclusion

A Section 85 rollover can be a powerful tool—but only when it’s planned and executed correctly. How you transfer assets into your corporation affects your tax position today and your flexibility in the future. Elections, valuations, and share structure all need to work together to achieve the intended outcome.

If you’re incorporating or transferring assets into a company, we can help you structure the rollover properly and align it with your long-term tax strategy.