Filing taxes late is one of the most common compliance issues Canadian business owners face. It’s rarely intentional. More often, it’s caused by delayed bookkeeping, cash flow pressure, or uncertainty around which tax deadlines actually apply.

The challenge is that the Canada Revenue Agency (CRA) doesn’t differentiate between why a filing is late. If a return is filed after the deadline—or taxes are not paid on time—penalties and interest can apply quickly. This blog explains which business taxes are due, when they’re due, how late filing penalties work, and what options exist if you’re already behind.

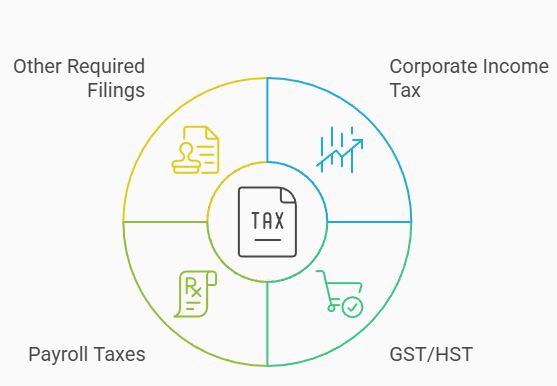

The Types of Taxes Canadian Businesses Are Responsible For

Most businesses deal with more than one type of tax. Missing any one of these deadlines can trigger penalties, interest, or CRA follow-up.

Corporate Income Tax

Corporations are required to file a T2 corporate tax return every year, even if:

- There is no tax owing

- The business is inactive

- The corporation incurred a loss

Failure to file on time can still create compliance issues, even when no tax is payable.

GST/HST

Businesses registered for GST/HST must file returns based on their assigned reporting period (monthly, quarterly, or annually).

Payroll Taxes

If you pay employees—or yourself through payroll—you must remit:

- CPP

- EI

- Income tax withholdings

These payroll source deductions are treated as trust money by CRA.

Other Required Filings

Many business owners are also responsible for:

- T4 and T5 slips

- Personal income tax (T1) returns

- Provincial sales taxes (such as PST or RST)

- Other information returns and elections

Late filing penalties can apply even when no tax is owed.

Key Filing and Payment Deadlines for Corporate Tax, GST, and Payroll

Each tax has its own deadline. Filing one on time does not protect you from penalties on another.

Corporate Tax Deadlines

- T2 filing deadline: 6 months after fiscal year-end

- Corporate tax payment deadline:

- Generally 2 or 3 months after year-end, depending on eligibility

It’s common for businesses to file on time but pay late—or vice versa. Both scenarios can result in penalties.

GST/HST Deadlines

- Monthly or quarterly filers: Return and payment due one month after period-end

- Annual filers:

- Return due three months after year-end

- Payment may be due earlier in some cases

Payroll Remittance Deadlines

Payroll remittances are usually due monthly or quarterly. Late payroll remittances are among the most aggressively penalized by CRA.

The Difference Between Filing a Return and Paying the Tax

This distinction is critical and often misunderstood.

- Filing late triggers late filing penalties

- Paying late triggers interest

- You can be penalized for one, the other, or both

Even if you cannot pay the balance owing, filing the return on time—or as soon as possible—is almost always the better option. Filing stops late filing penalties from continuing to accrue, even though interest will still apply.

For many business owners, this is where things stall. Uncertainty around how much is owed, which returns are outstanding, or which taxes to prioritize often leads to further delay. Addressing those questions early—before penalties compound—usually limits the overall cost and gives you more options when dealing with CRA.

How CRA Calculates Late Filing Penalties

CRA penalties depend on two factors:

- Whether the return was filed late

- Whether taxes were paid late or not paid at all

Late Filing Penalties When Tax Is Owing

If a return is filed late and tax is owed, CRA generally charges:

- 5% of the balance owing, plus

- 1% per month for each full month late

- Up to a maximum of 12 months

If a late filing penalty was applied in any of the previous three years, penalties increase to:

- 10% of the balance owing, plus

- 2% per month, up to 20 months

These penalties apply to both corporate and personal income tax returns.

Interest and Penalties for Unpaid or Partially Paid Taxes

If taxes are unpaid or only partially paid by the due date:

- CRA charges daily compounding interest

- Interest also applies to penalties once assessed

There is no grace period. Interest begins the day after the payment deadline and continues until the balance is fully paid.

Late Filing Penalties for GST/HST and Payroll

GST/HST Late Filing Penalties

When a GST/HST return is filed late and a balance is owing:

- 1% of the amount owing, plus

- 0.25% per month, up to 12 months

Interest is charged separately.

Payroll Late Remittance Penalties

Payroll penalties typically range from:

- 3% to 10% of the amount owing

- Higher penalties for repeated failures

Because payroll deductions are considered trust funds, enforcement is stricter.

Filing Obligations When the Business Has a Loss or a GST Refund

Corporate Losses

Even when a corporation has a loss:

- The T2 return must still be filed on time

- Losses can be carried forward or back

- Late filing can delay or restrict future tax planning

GST Refunds

If a GST refund is expected:

- Late filing penalties generally do not apply

- CRA will not issue the refund until the return is filed

- Repeated late filings can increase CRA scrutiny

Compliance still matters, even when money is coming back to the business.

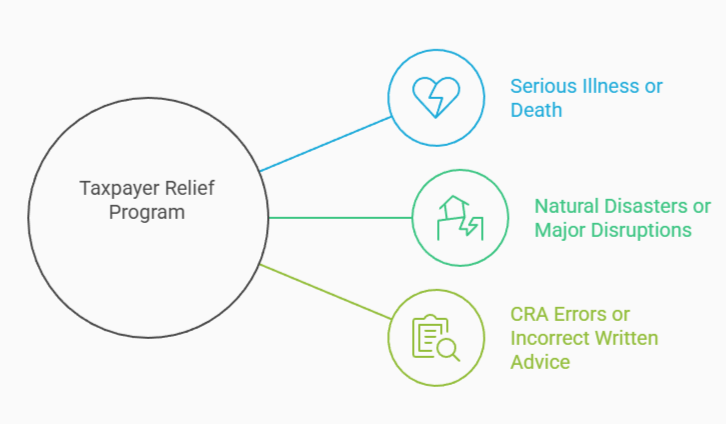

CRA Relief for Extraordinary Circumstances

CRA may cancel or reduce penalties and interest under the Taxpayer Relief Program when circumstances were beyond the taxpayer’s control.

Examples include:

- Serious illness or death

- Natural disasters or major disruptions

- CRA errors or incorrect written advice

Relief is not automatic, and CRA generally requires all outstanding returns to be filed before considering a request.

CRA Payment Arrangements for Businesses

When taxes cannot be paid in full, CRA may allow a payment arrangement.

A payment arrangement:

- Allows balances to be paid over time

- Does not eliminate interest

- Can reduce the risk of enforced collections if followed

CRA typically expects:

- All returns to be filed

- A realistic payment proposal

- Ongoing compliance once agreed

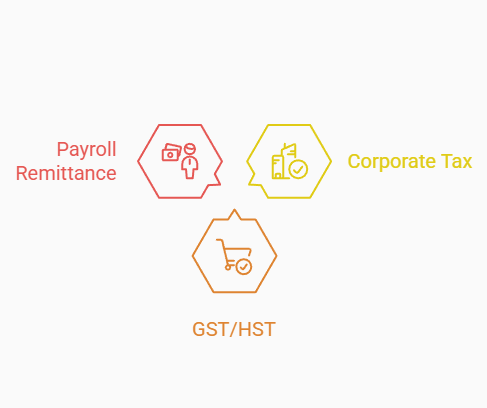

Prioritizing Payments When Cash Is Limited

When funds are tight, payment order matters.

Generally:

- Payroll remittances

- GST/HST

- Corporate income tax

This approach does not eliminate penalties or interest but can reduce exposure to the most serious enforcement actions.

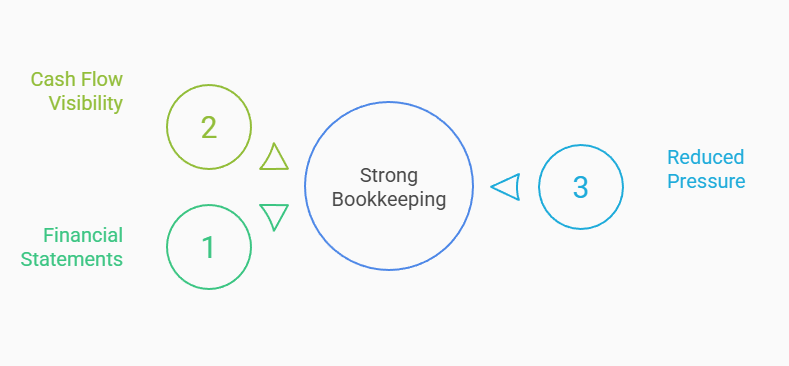

The Role of Good Bookkeeping in Avoiding Late Filing Issues

Late filings are often a bookkeeping issue rather than a tax issue.

Strong bookkeeping helps by:

- Keeping financial statements ready ahead of deadlines

- Improving cash flow visibility for tax planning

- Reducing last-minute filing pressure

Reduced Audit Risk

Accurate records:

- Support eligible business expenses

- Reduce ineligible or unsupported deductions

- Make CRA reviews more efficient

Maximized Deductions and Lower Taxes

Up-to-date bookkeeping:

- Ensures deductions and credits are captured

- Improves timing and planning opportunities

- Can directly reduce taxes owing

Frequently Asked Questions About Filing Taxes Late in Canada

Q: Is it better to file late or not file at all?

A: Filing late is almost always better than not filing. Filing stops late filing penalties from continuing to grow.

Q: Can CRA charge penalties if no tax is owing?

A: Late filing penalties usually apply only when tax is owed, but CRA still expects returns to be filed on time.

Q: Does filing late increase audit risk?

A: Repeated late filings can increase CRA scrutiny, especially when combined with poor bookkeeping or inconsistent reporting.

Q: Can penalties be waived if I can’t afford to pay?

A: Financial difficulty alone does not qualify for relief, but CRA may consider payment arrangements.

Q: How far back can CRA require unfiled returns?

A: CRA can require filings for multiple prior years, and unfiled returns often delay refunds or credits.

Conclusion

Late tax filings often stem from complex rules and overlapping deadlines—not inaction. Corporate tax, GST, and payroll each come with different requirements, and falling behind on one can quickly snowball into a bigger issue. The key is to file as soon as possible to limit penalties and keep your options open.

Purpose CPA helps Canadian business owners catch up on late filings, manage CRA penalties, and put systems in place to stay compliant. If you’re behind or unsure where you stand, contact us today!