The 2025 Federal Budget introduced several important tax updates that directly affect Canadian small business owners and incorporated professionals. Many of the previously proposed changes—especially around capital gains and compliance rules—have now been reversed or clarified.

For business owners planning equipment purchases, innovation investments, or future business sales, this budget restores stability and provides new opportunities to plan with confidence.

Here are the key updates that matter most to small business owners.

1. Underused Housing Tax (UHT) — Repealed

The federal government will eliminate the Underused Housing Tax (UHT).

This means that corporations, trusts, and partnerships that previously filed annual UHT returns to avoid penalties will no longer need to file once the repeal legislation is enacted.

Further details and the effective date will be announced in upcoming legislation.

2. Bare Trust Filing — Deferred

The new bare trust reporting requirements under the T3 regime have been deferred indefinitely.

After widespread confusion during the 2023 filing season, the CRA has chosen to pause enforcement while it re-evaluates the scope and intent of these filings. This means most informal or nominee arrangements that triggered T3 filings last year will not require immediate action for 2025.

3. Capital Gains Inclusion Rate — Back to 50%

The proposed increase in the capital gains inclusion rate from 50% to 66.7% has been cancelled.

Business owners selling shares, real estate, or other investments can continue to include only 50% of their capital gains in taxable income. This reversal restores planning certainty for entrepreneurs and investors considering future exits or restructurings.

4. Enhanced Capital Gains Exemption — Withdrawn

The government will not proceed with the proposed Entrepreneurs’ Incentive, which aimed to increase the capital gains exemption on qualifying small business shares.

The Lifetime Capital Gains Exemption (LCGE) remains at $1.25 million, and the standard qualification tests for Qualified Small Business Corporation (QSBC) shares continue to apply.

5. SR&ED Program — Capital Expenditures Now Eligible

The 2025 Budget reintroduces the ability to claim SR&ED tax credits on capital equipment used for scientific research and experimental development.

This means machinery, tooling, and technology directly used in innovation projects can now be partially funded through refundable or non-refundable SR&ED credits. It’s a significant policy shift that helps businesses reinvest in R&D and improve productivity without tying up as much cash flow.

6. 100% CCA (Full Expensing) Extended to 2030

Businesses can now claim a full deduction (100% CCA) in the year of purchase for eligible machinery, equipment, and new manufacturing buildings acquired and available for use up to 2030.

This extension aligns with other productivity incentives and allows companies to fully expense capital investments instead of spreading deductions over several years. It’s especially beneficial for manufacturers and growth-oriented businesses expanding their facilities or upgrading technology.

7. Carbon Tax Rebate — Now Non-Taxable

The Canada Carbon Rebate for Small Businesses will now be non-taxable.

This ensures rebate payments received from the government will not be included in taxable income.

It simplifies accounting and ensures that small businesses receive the full benefit of the rebate without additional tax implications.

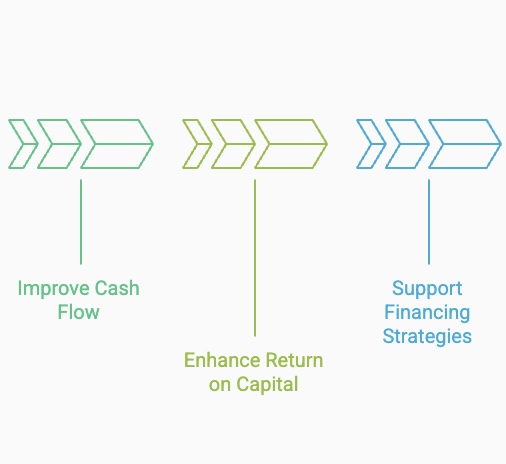

Integrating SR&ED and 100% CCA for Capital Planning

The combination of SR&ED tax credits and 100% CCA full expensing can dramatically reduce the after-tax cost of equipment and technology investments.

When properly coordinated, these measures can:

- Improve cash flow in the first year of an investment

- Enhance return on capital for manufacturing and R&D projects

- Support financing strategies that align with accelerated tax deductions

Learn more about how SR&ED and 100% CCA work together under Budget 2025.

Conclusion

Budget 2025 offers a welcome reset for small business owners. The elimination of the UHT, deferral of bare trust filings, and reinstatement of the 50% capital gains inclusion rate all simplify compliance and improve planning stability. Meanwhile, new opportunities under SR&ED and 100% CCA can make capital investments more affordable than ever—especially when planned strategically.

Need help understanding how the 2025 Federal Budget affects your business? Contact us today to navigate these changes, optimize your tax strategy, and plan your next move with confidence.