Securing bank financing is a major step for Canadian small businesses—but understanding the terms and documents involved can be overwhelming. From interest rates and repayment schedules to collateral and legal agreements, each component directly impacts your cash flow, risk exposure, and long-term growth.

Whether you’re applying for your first loan or refinancing existing debt, knowing how bank financing works—and what to watch for—can help you make more confident, informed decisions.

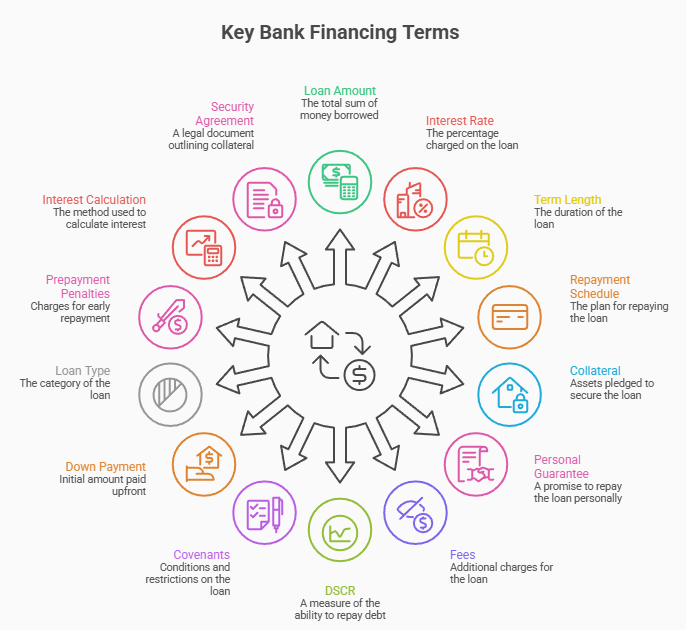

Key Bank Financing Terms Every Business Owner Should Understand

Before obtaining bank financing, Canadian small business owners need to understand key loan terms (like interest rates, repayment structure, and covenants), as well as legal documents such as term sheets, loan agreements, and security agreements. These determine your obligations, your risk exposure, and what happens if repayment terms aren’t met.

- Loan Amount: This is the total sum the bank will lend to your business. It’s the foundation of your financing and can determine the scale of your business activities or expansion plans.

- Interest Rate: The rate charged on the loan, which can either be fixed (constant) or variable (fluctuating with market conditions). Understanding the interest rate helps you calculate your long-term cost of borrowing.

- Term Length: This is the time over which you’ll repay the loan. Loan terms can range from short-term (1-3 years) to long-term (5-10 years or more).

- Repayment Schedule: Most loans require monthly repayments, but some might have flexible structures. Knowing when and how much you need to pay is key to managing cash flow.

- Collateral: This refers to assets—such as property, equipment, or inventory—that you pledge to the bank in case you default on the loan. It’s a way for the bank to secure its investment.

- Personal Guarantee: In some cases, the bank might ask for a personal guarantee from business owners. This means you could be personally liable for the loan if the business fails to repay it.

- Fees: Don’t forget to factor in extra costs like origination fees, application fees, or early repayment fees. Clarifying these upfront ensures you don’t encounter unexpected costs down the road.

- Debt Service Coverage Ratio (DSCR): This ratio helps the bank assess your business’s ability to repay debt. It’s calculated by dividing your operating income by your debt service. A higher ratio indicates a lower risk for the bank.

- Covenants and Restrictions: These are conditions imposed by the bank to protect its investment. Common examples include:

- Financial Covenants: Requirements to maintain certain financial ratios.

- Operational Covenants: Restrictions on business activities, like limiting capital expenditures.

- Reporting Covenants: Obligations to submit regular financial reports.

- Down Payment: Depending on the loan type, the bank might require a down payment to secure the loan. This is typically a percentage of the total loan amount.

- Loan Type: Banks offer various loan types, including term loans, lines of credit, and government-backed loans (like the Canada Small Business Financing Program (CSBFP)). Each loan type has specific conditions and terms.

- Prepayment Penalties: Some loans come with penalties if you pay them off early. If you’re considering repaying your loan ahead of schedule, make sure you understand any associated fees.

- Interest Calculation Method: Understand whether the interest is simple or compound and whether it’s calculated on the initial loan amount or a reducing balance.

- Security Agreement: This agreement outlines what assets are pledged as collateral, ensuring that the bank has recourse to recover its funds if you default.

If you’re unsure how loan terms or financing structure will impact your business, a professional review can help you assess risk, improve your position with lenders, and avoid costly surprises.

Term Sheet vs. Loan Agreement: What’s the Difference?

When applying for a loan, you’ll encounter both a term sheet and a loan agreement. These two documents play different roles in the lending process, and understanding the difference between them can save you time and stress.

Term Sheet

A term sheet is a non-binding document that outlines the key loan terms before a formal agreement is reached. It’s essentially a summary of the loan’s structure, including:

- Loan amount and interest rate.

- Repayment terms and schedule.

- Collateral requirements.

- Any covenants or restrictions the bank expects.

While the term sheet is an important starting point, it’s not legally binding, so it serves as the foundation for further negotiations and the eventual loan agreement.

Loan Agreement

A loan agreement is the binding contract that finalizes the loan terms. Once you sign this, you’re legally committed to the terms outlined, which can include:

- Loan amount and repayment terms.

- Collateral and specific assets pledged.

- Events of default (what happens if you miss payments).

- Legal clauses on dispute resolution and remedies for breach of contract.

This agreement is detailed and enforceable, ensuring both you and the bank are clear about your rights and obligations.

What Are Collateral and Security Agreements in Business Loans?

In most bank loans, particularly for small businesses, the lender will require a collateral agreement and security agreement to reduce risk. Here’s what each entails:

Collateral Agreement

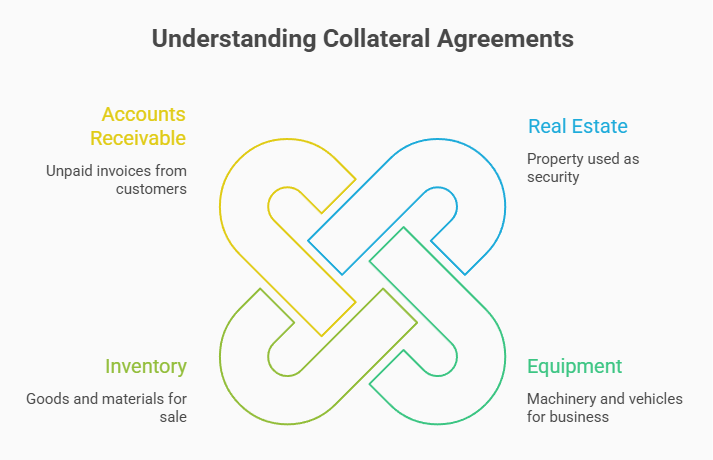

A collateral agreement is a legal document that specifies the assets you pledge to secure the loan. This could include:

- Real estate (e.g., commercial property).

- Equipment (e.g., machinery, vehicles).

- Inventory (e.g., goods or materials for sale).

- Accounts receivable (unpaid invoices from customers).

By signing this agreement, you allow the bank to seize these assets if you default on the loan, giving them a way to recover their investment.

Security Agreement

A security agreement goes hand in hand with the collateral agreement. It’s a more detailed contract that outlines the bank’s rights regarding the collateral and the process for recovering it in case of loan default. Key components of a security agreement include:

- A detailed description of the pledged collateral.

- Terms for what constitutes a default (e.g., missed payments).

- Rights and obligations of both parties concerning the collateral.

The security agreement gives the bank a legal claim to your business’s assets, ensuring they are protected if the loan terms aren’t met.

Conclusion

Understanding the structure of bank financing—from key terms to legal agreements—can make a significant difference in how confidently you approach borrowing. These details not only define your repayment obligations but also determine your financial flexibility and risk. Before committing to any financing arrangement, it’s important to fully understand what you’re signing and how it aligns with your business goals.

Not sure if your loan terms are structured in your best interest? A second look can help you identify risks, improve cash flow planning, and strengthen your financing strategy. Book a consultation with Purpose CPA to review your financing structure and make informed decisions with confidence.